Materiality in Finance: A Definition

Materiality, in the context of finance, refers to the significance of information. It dictates whether an omission or misstatement of financial information could reasonably influence the economic decisions of users of that information. In simpler terms, it’s about whether something is big enough to matter to investors, creditors, and other stakeholders when they’re making financial decisions.

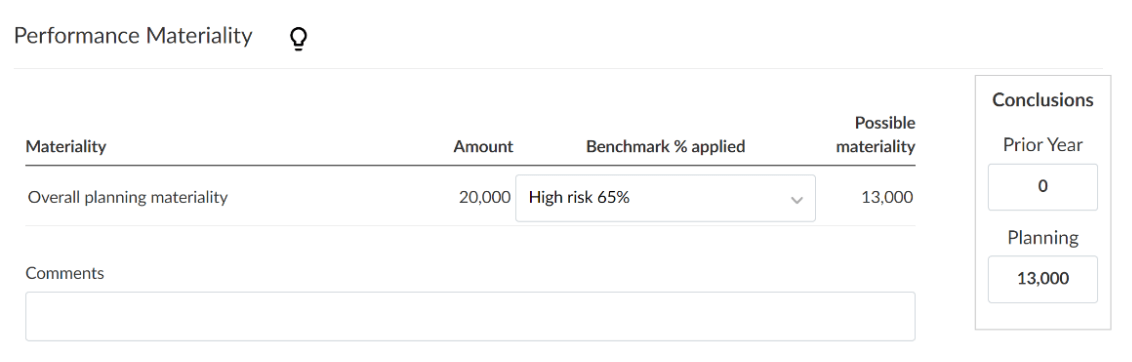

The concept of materiality isn’t about strict dollar amounts; it’s about relative significance. A $1,000 error might be immaterial for a multinational corporation with billions in revenue but could be highly material for a small startup with limited resources. This relative importance is often evaluated as a percentage of a key benchmark like revenue, net income, or total assets.

Several factors influence the determination of materiality. These include:

- Quantitative factors: This involves evaluating the size of the error or omission relative to a benchmark. While specific thresholds vary, auditors and companies often use rules of thumb, such as 5% of net income before taxes, to assess materiality quantitatively.

- Qualitative factors: Even if a misstatement is small in dollar terms, it might still be material due to its nature. For example, an illegal payment, even a small one, could be material because it indicates potential unethical behavior or legal violations. A misstatement that affects a company’s compliance with debt covenants, or that affects management compensation, can also be qualitatively material.

- Context: The circumstances surrounding the error or omission are crucial. A misstatement might be more material if it occurs in a period of high economic uncertainty or if the company is facing significant financial challenges.

Materiality is crucial for several reasons:

- Accurate Financial Reporting: It ensures that financial statements provide a fair and accurate representation of a company’s financial performance and position.

- Informed Decision-Making: It helps investors and other stakeholders make informed decisions by focusing on information that is most relevant to their assessments.

- Auditor’s Responsibility: Auditors use materiality to plan and perform their audits effectively. They focus on identifying and addressing misstatements that could be material to the financial statements.

- Legal and Regulatory Compliance: Material misstatements can have legal and regulatory consequences. Companies and their management can face penalties for failing to disclose material information.

Ultimately, determining materiality is a matter of professional judgment. Auditors, accountants, and management teams must consider both quantitative and qualitative factors, along with the specific circumstances of the company, to decide whether information is material enough to influence the decisions of a reasonable investor. It’s a critical aspect of maintaining the integrity and reliability of financial reporting.

2190×1146 materiality definition ultimate guide datamaran from www.datamaran.com

2190×1146 materiality definition ultimate guide datamaran from www.datamaran.com  940×789 materiality concept significance abuse efinancemanagement from efinancemanagement.com

940×789 materiality concept significance abuse efinancemanagement from efinancemanagement.com  600×400 materiality accounting play from accountingplay.com

600×400 materiality accounting play from accountingplay.com  1100×596 materiality principle accounting definition coinranking from cryptolisting.org

1100×596 materiality principle accounting definition coinranking from cryptolisting.org  1024×683 materiality akgvg associates from www.akgvg.com

1024×683 materiality akgvg associates from www.akgvg.com  1024×766 accounting concepts completeness neutrality accounting corner from accountingcorner.org

1024×766 accounting concepts completeness neutrality accounting corner from accountingcorner.org  512×512 materiality concept accounting definition eduyush from eduyush.com

512×512 materiality concept accounting definition eduyush from eduyush.com  1201×652 materiality assessment csrd requirement from endure-consulting.com

1201×652 materiality assessment csrd requirement from endure-consulting.com  2135×595 materiality bipartisan policy center from bipartisanpolicy.org

2135×595 materiality bipartisan policy center from bipartisanpolicy.org  1200×290 materiality nifco from www.nifco.com

1200×290 materiality nifco from www.nifco.com  684×384 materiality concept definition examples importance advantages from www.wallstreetmojo.com

684×384 materiality concept definition examples importance advantages from www.wallstreetmojo.com  640×442 recommended materiality accounting trullion from trullion.com

640×442 recommended materiality accounting trullion from trullion.com  585×439 materiality from whitecollaraccountant.com

585×439 materiality from whitecollaraccountant.com  1024×581 esg materiality maps navigating sustainable finance from sustainablecapitalgroup.com

1024×581 esg materiality maps navigating sustainable finance from sustainablecapitalgroup.com  1190×1540 materiality concept audit financial statements desklib from desklib.com

1190×1540 materiality concept audit financial statements desklib from desklib.com  2188×1322 materiality priority key challenges sustainability mitsubishi hc from www.mitsubishi-hc-capital.com

2188×1322 materiality priority key challenges sustainability mitsubishi hc from www.mitsubishi-hc-capital.com  1280×720 materiality superfastcpa cpa review from www.superfastcpa.com

1280×720 materiality superfastcpa cpa review from www.superfastcpa.com  1400×788 apply accounting materiality concept steps purpose from www.business-case-analysis.com

1400×788 apply accounting materiality concept steps purpose from www.business-case-analysis.com  1200×630 materiality finance interview sarah besky society from culanth.org

1200×630 materiality finance interview sarah besky society from culanth.org  620×200 materiality accounting hbs from online.hbs.edu

620×200 materiality accounting hbs from online.hbs.edu  720×931 materiality concept powerpoint id from www.slideserve.com

720×931 materiality concept powerpoint id from www.slideserve.com  1174×1030 materiality financial analysis modeling magnimetrics from magnimetrics.com

1174×1030 materiality financial analysis modeling magnimetrics from magnimetrics.com  1551×1373 double materiality assessment from go.uprightproject.com

1551×1373 double materiality assessment from go.uprightproject.com  1132×362 define materiality from docs.caseware.com

1132×362 define materiality from docs.caseware.com  638×903 materiality principle accounting from www.online-accounting.net

638×903 materiality principle accounting from www.online-accounting.net  474×314 materiality accounting cruseburke from cruseburke.co.uk

474×314 materiality accounting cruseburke from cruseburke.co.uk  640×427 understanding materiality concept accounts from www.backoffice.com.sg

640×427 understanding materiality concept accounts from www.backoffice.com.sg  504×523 materiality concept accounting kaiyaqokline from kaiyaqokline.blogspot.com

504×523 materiality concept accounting kaiyaqokline from kaiyaqokline.blogspot.com  1845×970 demystifying double materiality debate paia consulting from paiaconsulting.com.sg

1845×970 demystifying double materiality debate paia consulting from paiaconsulting.com.sg