Lower Partial Moments (LPMs) are risk measures that focus specifically on the negative deviations of an investment’s returns from a specified target or threshold. Unlike traditional risk measures like standard deviation, which penalize both positive and negative deviations equally, LPMs only consider returns that fall below the target return. This makes them particularly attractive to investors who are more concerned with downside risk than upside potential.

The core idea behind LPMs is rooted in behavioral finance, which recognizes that individuals often exhibit asymmetric preferences regarding gains and losses. People tend to feel the pain of a loss more acutely than the pleasure of an equivalent gain. Therefore, a risk measure that disproportionately weights losses provides a more realistic assessment of perceived risk. Think of it this way: an investor might be perfectly happy with significant upside volatility, but extremely averse to any chance of falling below a certain retirement income target. LPMs can capture this type of aversion.

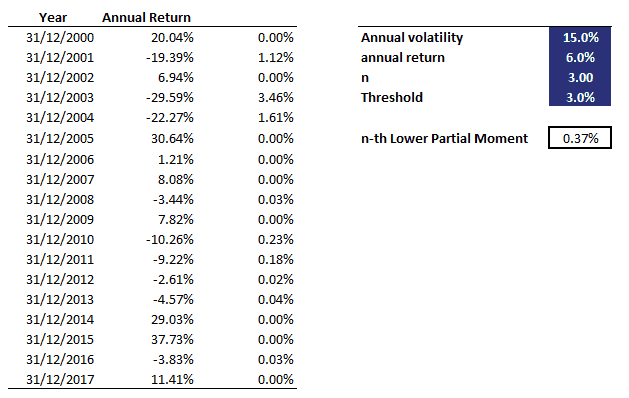

There are several different types of LPMs, distinguished by the power to which the negative deviations are raised. The most common are:

- First-Order LPM (LPM1): Also known as the “mean shortfall,” this measures the average magnitude of the deviations below the target. It simply calculates the average difference between the target return and the actual return, but only considers instances where the actual return is less than the target.

- Second-Order LPM (LPM2): This is similar to variance, but it only considers the squared deviations below the target. It provides a measure of the “downside variance” and is often used as a downside risk equivalent to standard deviation. It is also equivalent to the square root of the Mean Square Error.

- Higher-Order LPMs (LPM3, LPM4, etc.): These raise the negative deviations to higher powers. As the order increases, the LPM becomes more sensitive to extreme negative returns, emphasizing the tail risk of the distribution. Higher-order LPMs penalize returns further below the target more heavily.

The target return used in calculating LPMs is crucial. It can represent various benchmarks, such as the risk-free rate, the average market return, or a specific return objective set by the investor. The choice of target significantly impacts the resulting LPM value and, consequently, the risk assessment.

LPMs are used in a variety of financial applications, including portfolio optimization, performance evaluation, and risk management. For example, in portfolio optimization, an investor might seek to minimize the LPM2 (downside variance) for a given level of expected return, effectively creating a portfolio that minimizes the risk of falling below the desired return. In performance evaluation, LPMs can be used to compare the downside risk of different investment strategies or fund managers, focusing on their ability to protect against losses.

While LPMs offer a more nuanced approach to risk assessment than traditional measures, they are not without their limitations. Calculating LPMs can be computationally intensive, especially for large datasets or complex portfolios. Furthermore, the choice of target return can be somewhat arbitrary and influence the outcome. Despite these limitations, LPMs remain a valuable tool for investors seeking a more comprehensive understanding of downside risk.

400×567 conditional partial moments framework erm symposium from www.yumpu.com

400×567 conditional partial moments framework erm symposium from www.yumpu.com  629×398 partial moment implementation excel from breakingdownfinance.com

629×398 partial moment implementation excel from breakingdownfinance.com  406×589 partial moments from www.finderandkeeper.co.uk

406×589 partial moments from www.finderandkeeper.co.uk  600×776 partial moments proxy downside risk from www.academia.edu

600×776 partial moments proxy downside risk from www.academia.edu  850×289 partial moments lpm benchmarks from www.researchgate.net

850×289 partial moments lpm benchmarks from www.researchgate.net  768×994 partial moments measures perceived risk from studylib.net

768×994 partial moments measures perceived risk from studylib.net  298×386 fillable tspace library utoronto sample expected from www.pdffiller.com

298×386 fillable tspace library utoronto sample expected from www.pdffiller.com  298×386 fillable portfolio selection partial moments fax email from www.pdffiller.com

298×386 fillable portfolio selection partial moments fax email from www.pdffiller.com  1000×565 partial dentures questions answered from northernriversdentureclinic.com.au

1000×565 partial dentures questions answered from northernriversdentureclinic.com.au  956×954 partial differential equations pdes finance economics markets from marketsportfolio.com

956×954 partial differential equations pdes finance economics markets from marketsportfolio.com  707×321 solved question distinction partial cheggcom from www.chegg.com

707×321 solved question distinction partial cheggcom from www.chegg.com  850×1200 role partial moments stochastic modeling from www.researchgate.net

850×1200 role partial moments stochastic modeling from www.researchgate.net  1350×536 table partial moments measures perceived risk from www.semanticscholar.org

1350×536 table partial moments measures perceived risk from www.semanticscholar.org  595×842 partial moments measure vulnerability poverty from www.academia.edu

595×842 partial moments measure vulnerability poverty from www.academia.edu  850×199 minimising ratios partial moments table from www.researchgate.net

850×199 minimising ratios partial moments table from www.researchgate.net  768×994 partial moments gram charlier distribution from studylib.net

768×994 partial moments gram charlier distribution from studylib.net  320×320 upper partial moments project hour tasks from www.researchgate.net

320×320 upper partial moments project hour tasks from www.researchgate.net  850×842 optimal partial moment hedge ratios table from www.researchgate.net

850×842 optimal partial moment hedge ratios table from www.researchgate.net  606×656 portfolio partial moment quadratic programming table from www.researchgate.net

606×656 portfolio partial moment quadratic programming table from www.researchgate.net  397×294 comparison partial moments top site af correlations from www.researchgate.net

397×294 comparison partial moments top site af correlations from www.researchgate.net  850×617 partial moment quadratic programming analysis degree from www.researchgate.net

850×617 partial moment quadratic programming analysis degree from www.researchgate.net