COI Finance, often referred to as Certificate of Insurance Finance or Insurance Premium Finance, is a financial product designed to help businesses manage their insurance costs by spreading premium payments over a defined period, typically six to twelve months. Instead of paying the entire insurance premium upfront, a company can secure financing to make monthly installments, allowing them to conserve working capital and better manage their cash flow.

The process involves a lending institution, often a specialized finance company, paying the insurance company the full premium on behalf of the insured. The insured then repays the finance company in installments, plus interest and any associated fees. The insurance policy itself serves as collateral for the loan. If the insured defaults on the payments, the finance company can cancel the policy and recoup the unearned premium directly from the insurance company.

Several benefits accrue from utilizing COI Finance. Firstly, it frees up significant capital that would otherwise be tied up in a large lump-sum insurance payment. This capital can then be reinvested in other areas of the business, such as operations, marketing, or expansion, potentially leading to higher returns than would be achieved by simply holding the cash. Secondly, it improves cash flow management. Predictable monthly payments allow for more accurate budgeting and forecasting. This can be particularly helpful for businesses with seasonal revenue fluctuations or those experiencing rapid growth.

Beyond financial flexibility, COI Finance can also offer some tax advantages. The interest paid on the financing may be tax-deductible, reducing the overall cost of insurance. Consult with a tax advisor to determine eligibility for these deductions. Furthermore, insurance coverage is secured immediately. The business is protected from potential liabilities from the moment the policy is in effect, without having to wait until the full premium is paid.

However, there are also potential drawbacks to consider. The primary cost is the interest rate charged on the financed premium. While freeing up capital is beneficial, the business will ultimately pay more for the insurance policy than if it had paid upfront. The interest rates can vary depending on the creditworthiness of the business, the size of the premium, and the prevailing market conditions. It’s crucial to carefully compare the costs and benefits of financing versus paying in full. Another risk is policy cancellation due to default. Failure to make timely payments can result in the insurance policy being canceled, leaving the business uninsured and vulnerable to potential liabilities. Due diligence is paramount. Businesses should thoroughly research and compare different financing options before committing to a COI Finance agreement.

In conclusion, COI Finance provides a valuable tool for businesses seeking to manage their insurance costs and improve their cash flow. While it offers significant advantages in terms of financial flexibility and capital preservation, it’s important to carefully weigh the costs and risks before deciding if it’s the right solution for a particular business.

1950×2850 report from www.culturalnavigator.com

1950×2850 report from www.culturalnavigator.com  800×335 insurance from mycoitracking.com

800×335 insurance from mycoitracking.com  1000×760 flat accounting logo design white background creative from stock.adobe.com

1000×760 flat accounting logo design white background creative from stock.adobe.com  768×1267 meaning origin examples esl from 7esl.com

768×1267 meaning origin examples esl from 7esl.com  474×248 meaning stand esl from 7esl.com

474×248 meaning stand esl from 7esl.com  1000×667 expensive mycoi from mycoitracking.com

1000×667 expensive mycoi from mycoitracking.com  1200×900 meaning fluentslang from fluentslang.com

1200×900 meaning fluentslang from fluentslang.com  875×497 certificate insurance definition contents management from www.financestrategists.com

875×497 certificate insurance definition contents management from www.financestrategists.com  800×335 mycoi from mycoitracking.com

800×335 mycoi from mycoitracking.com  1000×941 share price company information asxcoi from www.asx.com.au

1000×941 share price company information asxcoi from www.asx.com.au  1200×943 meaning slangorg from www.slang.org

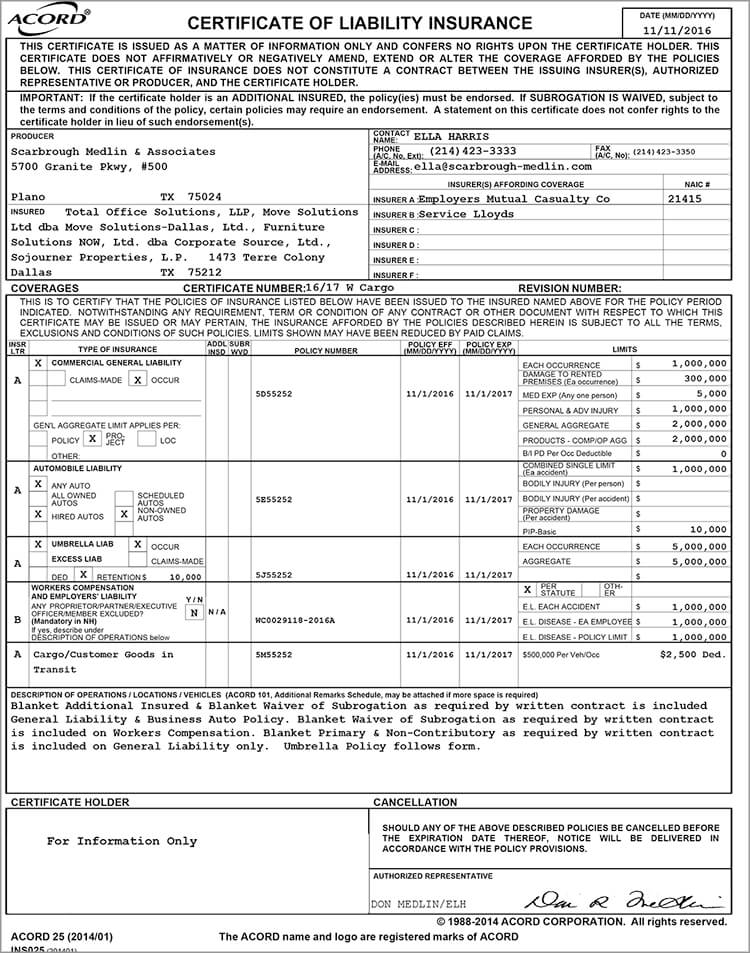

1200×943 meaning slangorg from www.slang.org  750×953 sample move solutions from www.movesolutions.com

750×953 sample move solutions from www.movesolutions.com  800×335 real estate from mycoitracking.com

800×335 real estate from mycoitracking.com  624×702 meaning origin popularity from www.momjunction.com

624×702 meaning origin popularity from www.momjunction.com  1620×2096 solution english studypool from www.studypool.com

1620×2096 solution english studypool from www.studypool.com  700×400 whats missing piece decision making puzzle from gihanperera.com

700×400 whats missing piece decision making puzzle from gihanperera.com  960×720 annual meeting japanese society from www.congre.co.jp

960×720 annual meeting japanese society from www.congre.co.jp  670×349 definition certificate insurance abbreviation finder from www.abbreviationfinder.org

670×349 definition certificate insurance abbreviation finder from www.abbreviationfinder.org  474×266 kunekune pigs from kunekunepigsforsale.net

474×266 kunekune pigs from kunekunepigsforsale.net  700×400 roi cost gihan perera futurist from gihanperera.com

700×400 roi cost gihan perera futurist from gihanperera.com  768×1024 coiph modern japanese staycation awesome awesome planet from awesome.blog

768×1024 coiph modern japanese staycation awesome awesome planet from awesome.blog  1024×640 full form from leverageedu.com

1024×640 full form from leverageedu.com  1200×628 full form insurance insurance meaning from insurerguru.com

1200×628 full form insurance insurance meaning from insurerguru.com