Robust statistics in finance addresses the limitations of traditional statistical methods when dealing with data containing outliers or deviations from assumed distributions. Financial data, characterized by market crashes, unexpected news, and trading errors, often violates the assumptions of normality and homogeneity, leading to biased estimates and unreliable conclusions if standard techniques are employed. Robust methods aim to mitigate the influence of these data anomalies, providing more stable and accurate insights.

A primary goal of robust statistics is to reduce the impact of outliers on parameter estimation. Consider the estimation of the average return of a stock. A single day with an extremely large price fluctuation can unduly influence the sample mean, leading to a misleading representation of typical returns. Robust estimators, such as the median or trimmed mean, are less sensitive to these extreme values. The median, for instance, is completely unaffected by outliers, making it a robust measure of central tendency. Trimmed means involve removing a certain percentage of the extreme values from both ends of the data before calculating the mean, providing a compromise between efficiency and robustness.

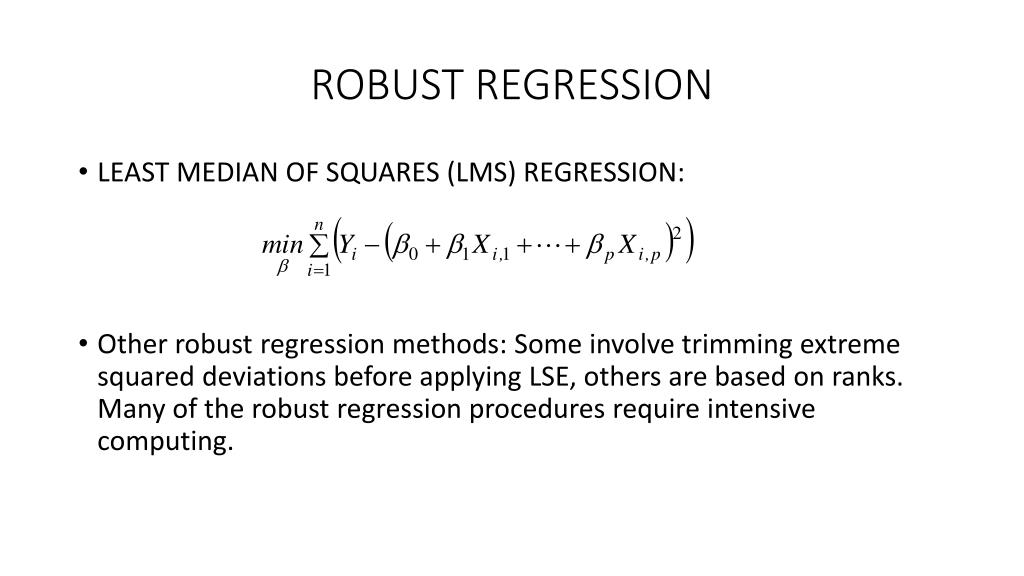

Beyond simple descriptive statistics, robust regression techniques are widely used in financial modeling. Ordinary Least Squares (OLS) regression, a staple in finance, is highly susceptible to outliers. Robust regression methods, like M-estimation, S-estimation, and MM-estimation, employ different weighting schemes to downweight the influence of outliers on the regression coefficients. M-estimators minimize a function of the residuals that is less sensitive to large errors than the squared errors used in OLS. S-estimators minimize a robust scale estimate of the residuals, while MM-estimators combine the advantages of both M and S-estimators. These techniques provide more reliable estimates of relationships between financial variables, even in the presence of noisy data.

Robust covariance matrix estimation is crucial for portfolio optimization and risk management. The sample covariance matrix, commonly used to quantify asset dependencies, can be severely distorted by outliers, leading to inaccurate portfolio allocations and underestimated risk. Robust covariance estimators, such as the Minimum Covariance Determinant (MCD) estimator and shrinkage estimators, provide more stable estimates of the covariance structure. The MCD estimator identifies a subset of the data that yields the lowest sample covariance determinant, effectively removing outliers. Shrinkage estimators combine the sample covariance matrix with a structured estimator, such as the identity matrix, to improve stability and reduce estimation error.

The application of robust statistics extends to various areas in finance. In asset pricing, robust regression models can be used to test factor models, providing more reliable evidence of risk premia. In risk management, robust volatility estimation techniques, such as the Huber estimator, are employed to calculate Value-at-Risk (VaR) and Expected Shortfall (ES), offering more accurate assessments of potential losses. Furthermore, robust methods can be used for anomaly detection, identifying unusual market behavior that may warrant further investigation.

In conclusion, robust statistics offer a valuable toolkit for analyzing financial data. By mitigating the influence of outliers and deviations from distributional assumptions, these techniques provide more reliable estimates, improved model performance, and better-informed decision-making in various financial applications.

261×361 robust statistics from onlybooks.org

261×361 robust statistics from onlybooks.org  576×384 robust statistics statistics jim from statisticsbyjim.com

576×384 robust statistics statistics jim from statisticsbyjim.com  436×648 robust statistics alchetron social encyclopedia from alchetron.com

436×648 robust statistics alchetron social encyclopedia from alchetron.com  1920×1080 corporate finance robust financial modeling career connections from connections.villanova.edu

1920×1080 corporate finance robust financial modeling career connections from connections.villanova.edu  335×499 main books robust statistics andrey akinshin from aakinshin.net

335×499 main books robust statistics andrey akinshin from aakinshin.net  300×117 robust statistics definition examples assumptions applications from www.wallstreetmojo.com

300×117 robust statistics definition examples assumptions applications from www.wallstreetmojo.com  1024×576 robust statistics powerpoint id from www.slideserve.com

1024×576 robust statistics powerpoint id from www.slideserve.com  1280×720 robust statistics powerpoint google cpb from www.slidegeeks.com

1280×720 robust statistics powerpoint google cpb from www.slidegeeks.com  232×372 robust statistics theory methods ricardo from pdfdrive.to

232×372 robust statistics theory methods ricardo from pdfdrive.to  2048×1056 statistics finance definition applications importance from corporatefinanceinstitute.com

2048×1056 statistics finance definition applications importance from corporatefinanceinstitute.com  1200×675 robustus finance ux case study behance from www.behance.net

1200×675 robustus finance ux case study behance from www.behance.net  850×1202 tutorial robust statistics from www.researchgate.net

850×1202 tutorial robust statistics from www.researchgate.net  1484×1252 robust statistics australian institute machine learning aiml from www.adelaide.edu.au

1484×1252 robust statistics australian institute machine learning aiml from www.adelaide.edu.au  1024×768 robust statistics portfolio construction powerpoint from www.slideserve.com

1024×768 robust statistics portfolio construction powerpoint from www.slideserve.com  1400×362 robust security measures modern finance companies behance from www.behance.net

1400×362 robust security measures modern finance companies behance from www.behance.net  320×320 figure stage robust statistic figure displays robust from www.researchgate.net

320×320 figure stage robust statistic figure displays robust from www.researchgate.net  850×796 generalized framework robust statistics scientific diagram from www.researchgate.net

850×796 generalized framework robust statistics scientific diagram from www.researchgate.net  1024×768 robust powerpoint id from www.slideserve.com

1024×768 robust powerpoint id from www.slideserve.com  2560×1280 robust financial stability believers ias academy from believersias.com

2560×1280 robust financial stability believers ias academy from believersias.com /GettyImages-678819921-63fd5512137043af809553f52b14990d.jpg) 2121×1414 robust from www.investopedia.com

2121×1414 robust from www.investopedia.com  1024×768 robust statistics norms powerpoint from www.slideserve.com

1024×768 robust statistics norms powerpoint from www.slideserve.com  363×363 robust financing policy scientific diagram from www.researchgate.net

363×363 robust financing policy scientific diagram from www.researchgate.net  626×352 premium ai image robust financial sector security from www.freepik.com

626×352 premium ai image robust financial sector security from www.freepik.com  850×165 summary robust regression scientific diagram from www.researchgate.net

850×165 summary robust regression scientific diagram from www.researchgate.net  614×614 shows statistics type finance demand from www.researchgate.net

614×614 shows statistics type finance demand from www.researchgate.net  606×355 quick tips business financially robust jcountcom from www.jcount.com

606×355 quick tips business financially robust jcountcom from www.jcount.com  1920×729 build robust financial plan case study rbc brewin dolphin from www.brewin.co.uk

1920×729 build robust financial plan case study rbc brewin dolphin from www.brewin.co.uk