Dividend finance, also known as dividend recapitalization, is a leveraged financing strategy where a company takes on new debt to pay a large, one-time dividend to its equity holders, typically private equity sponsors. Unlike regular dividend payouts funded by ongoing earnings, dividend finance involves borrowing money specifically for the purpose of distributing cash to shareholders.

How it Works:

- A company, often one owned by a private equity firm, assesses its financial position and identifies an opportunity to leverage its assets.

- Investment bankers are engaged to structure and arrange the financing. They analyze the company’s cash flow, debt capacity, and overall financial health to determine the amount of debt the company can realistically support.

- The company issues new debt, usually in the form of loans or high-yield bonds. This debt is secured by the company’s assets.

- The proceeds from the new debt are used to pay a substantial dividend to the equity holders. This dividend is typically a multiple of the company’s regular dividend payout, if any.

- The company is now burdened with the new debt and must service the debt through its ongoing cash flows.

Motivations for Dividend Finance:

- Returns for Private Equity: The primary driver is often to provide a quick return on investment for private equity sponsors. It allows them to extract capital from the company before a potential sale or IPO.

- Increase Shareholder Value: A dividend recapitalization can signal confidence in the company’s future performance, potentially increasing its perceived value.

- Optimize Capital Structure: In some cases, dividend finance can be used to rebalance the company’s capital structure, increasing the proportion of debt.

- Tax Advantages: Depending on the tax jurisdiction, dividend payments may be taxed differently than capital gains, making dividend finance a tax-efficient way to return capital.

Risks and Considerations:

- Increased Leverage: The most significant risk is the increased financial burden on the company. The company’s cash flow must be sufficient to cover the debt service, leaving less available for reinvestment, research and development, or weathering economic downturns.

- Financial Distress: Overleveraging can significantly increase the risk of financial distress and potential bankruptcy, especially if the company’s performance deteriorates.

- Agency Costs: Dividend finance can create conflicts of interest between shareholders (who receive the dividend) and bondholders (who bear the risk of default).

- Market Perception: While intended to boost perceived value, a dividend recapitalization can sometimes be viewed negatively by the market, especially if the company is already heavily leveraged.

In conclusion, dividend finance can be a strategic tool for companies seeking to return capital to shareholders, particularly in the private equity context. However, it is crucial to carefully assess the potential risks and ensure the company’s financial health can withstand the increased leverage before pursuing this strategy. The decision to engage in dividend finance should be based on a thorough evaluation of the company’s long-term prospects and its ability to service the additional debt.

2000×1013 dividend finance from www.dividendfinance.com

2000×1013 dividend finance from www.dividendfinance.com  1160×1160 dividend napkin finance from napkinfinance.com

1160×1160 dividend napkin finance from napkinfinance.com  1200×800 dividend investing work thestreet from www.thestreet.com

1200×800 dividend investing work thestreet from www.thestreet.com  600×620 dividend fitness finance royalty images stock pictures from www.shutterstock.com

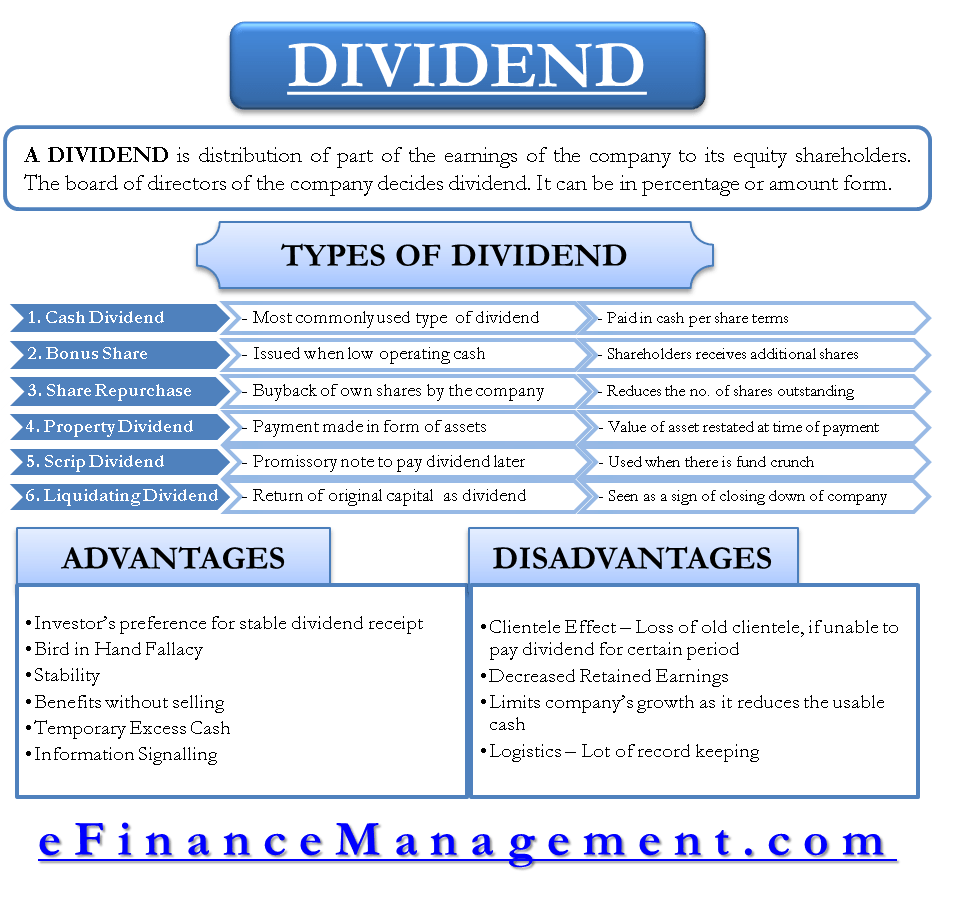

600×620 dividend fitness finance royalty images stock pictures from www.shutterstock.com  958×904 dividends forms advantages disadvantages efm from efinancemanagement.com

958×904 dividends forms advantages disadvantages efm from efinancemanagement.com  1200×627 dividend finance closes million solar loan securitization from www.businesswire.com

1200×627 dividend finance closes million solar loan securitization from www.businesswire.com  800×285 dividend stocks steps high dividend investing from learn.synvestable.com

800×285 dividend stocks steps high dividend investing from learn.synvestable.com  968×800 dividend income feb from financesmiths.com

968×800 dividend income feb from financesmiths.com  1024×653 guide dividend investing singapore investors syfe from www.syfe.com

1024×653 guide dividend investing singapore investors syfe from www.syfe.com  1200×675 dividend yield top dividend paying stocks nifty smallcap from www.goodreturns.in

1200×675 dividend yield top dividend paying stocks nifty smallcap from www.goodreturns.in  960×540 amp share dividend rivy courtney from jennableanor.pages.dev

960×540 amp share dividend rivy courtney from jennableanor.pages.dev  2560×1440 singapore dividend stocks steady dividends years from www.drwealth.com

2560×1440 singapore dividend stocks steady dividends years from www.drwealth.com  1024×586 safely build global dividend portfolio singapore from www.dividendtitan.com

1024×586 safely build global dividend portfolio singapore from www.dividendtitan.com  1024×683 ultimate guide dividend investing finplan from finplanco.com

1024×683 ultimate guide dividend investing finplan from finplanco.com  1500×1000 dividend growth stocks buy dividendinvestorcom from www.dividendinvestor.com

1500×1000 dividend growth stocks buy dividendinvestorcom from www.dividendinvestor.com :max_bytes(150000):strip_icc()/understanding-dividend-yield-3140782_final-076786b7660f49e7b4c2250a47bca173.png) 1500×1000 understanding dividend yield calculate from www.thebalancemoney.com

1500×1000 understanding dividend yield calculate from www.thebalancemoney.com  1536×603 dividend investing basics virk media from mrvirk.com

1536×603 dividend investing basics virk media from mrvirk.com  1024×640 dividend stock money eh from moneyeh.ca

1024×640 dividend stock money eh from moneyeh.ca  1560×880 limited companies invest dividend fund global from www.foxymonkey.com

1560×880 limited companies invest dividend fund global from www.foxymonkey.com  767×460 dividend cmc invest from www.cmcinvest.com

767×460 dividend cmc invest from www.cmcinvest.com  936×540 quick guide dividend investing from insights.endowus.com

936×540 quick guide dividend investing from insights.endowus.com  1536×1025 dividend investing singapore complete guide from dollarbureau.com

1536×1025 dividend investing singapore complete guide from dollarbureau.com  1919×1281 dividend stocks singapore selections from dollarbureau.com

1919×1281 dividend stocks singapore selections from dollarbureau.com  1200×675 rs share dividends months high dividend paying stocks hit from www.goodreturns.in

1200×675 rs share dividends months high dividend paying stocks hit from www.goodreturns.in  2240×1260 key metrics dividend investing prosperus from www.prosperus.asia

2240×1260 key metrics dividend investing prosperus from www.prosperus.asia  1280×720 dividend stocks dividend invest dividend stocks from www.timesnownews.com

1280×720 dividend stocks dividend invest dividend stocks from www.timesnownews.com  5791×3412 dividend paying stocks singaporehawk insight from www.hawkinsight.com

5791×3412 dividend paying stocks singaporehawk insight from www.hawkinsight.com  1792×1024 high dividend stocks balancing yield risk from fncmx.com

1792×1024 high dividend stocks balancing yield risk from fncmx.com  2000×1190 complete guide dividend investing australia from getbamboo.com.au

2000×1190 complete guide dividend investing australia from getbamboo.com.au